Your premier partner in sports law & tax

#sportslaw #tax #socialsecurity

Friday, 7 January 2022 – The Belgian government’s intention to reform the current tax and social security regime for athletes and clubs has materialized in a number of concrete changes to the existing legal framework. The measures, adopted in the framework of the latest budget agreement aim to raise another 43 MEUR worth of income for the Belgian state.

Until now, athletes enjoy a specific regime with limited social security benefits and limited social security contributions. Contrary to what’s the case for a regular employee, the social security contributions payable for a professional athlete are currently calculated on a capped amount of 2,425.64 EUR. As a result, the total amount of social security contributions for a professional athlete amounts to less than 1,000 EUR per month, irrespective of the global salary of the athlete. For some time now, this limited social security contribution has sparked public outrage.

As from 1 January 2022, professional athletes will fall entirely within the scope of the regular social security regime for employees. They will enjoy regular social security benefits, but will also be subject to the regular social security contributions. As a result, as from 1 January 2022, 13.07% employee contributions will be withheld from the athlete’s gross salary) and 25% employer contributions will have to be paid on top of the gross salary (and a 1.69% special employer contribution). Specific rates apply for young athletes.

“As from 1 January 2022, professional athletes will fall entirely within the scope of the regular social security regime for employees”

To cushion the blow somewhat, the government will adopt reductions of both employee and employer contributions. For employee contributions, a lump sum amount of 281.73 EUR (137.81 EUR for athletes who, in the course of the calendar year, have not at least reached 19 years of age) is announced. In addition, a 60% reduction on the remaining part of the employee contributions is foreseen. For employer contributions, a reduction of 65% of the employer contributions has been agreed to.

Specific reductions are foreseen for employees with low monthly gross salaries.

It remains to be seen, in the framework of future budget rounds, whether this compensation will be temporary or not.

The following tax measures have taken effect as of 1 January 2022:

As a general rule, employers must withhold wage tax on the salaries paid to their athletes – employees. The wage withholding tax is a prepayment of the personal income tax liability of the athletes. Up to 31 December 2021, employers of athletes enjoyed an 80% wage tax exemption, meaning that employers were exempt from paying on 80% of the wage tax withheld to the tax authorities.

The wage tax exemption applied to salaries paid to +26yrs athletes is subject to a number of conditions, one of which being that the employer should reinvest 50% of the exempt wage tax in the education of u23 athletes.

The budget reform now provides in a reduction of the exemption rate from 80% to 75%. On top, the reinvestment ratio is increased to 55%.

“The budget reform provides in a reduction of the exemption rate from 80% to 75% and increases the reinvestment ratio to 55%.”

This measure is less far-reaching than the initial proposal of the Belgian Minister of Finance, who was aiming for a 4M EUR wage tax exemption cap for each employer. Since one of the main drivers of the Minister of Finance is to further align the tax regime with EU State Aid regulations, the Belgian government has already announced to revisit the wage tax exemption regime for sports teams in the course of 2022, potentially involving an in-depth review of the reinvestment obligations.

The existing flat tax rate of 16.5% applicable to the first 20.520 EUR (income year 2021) earned by U26 athletes will now become exclusive to U23 athletes. Transitional measures apply to athletes aging between 23 yrs and 26 yrs on 1 January 2022.

The possibility of an early withdrawal of supplementary pensions by athletes as of the age of 35 is eliminated. For more information, click here.

Agent’s fees in excess of 3% of an athlete’s gross annual salary will no longer be tax deductible in the hands of the paying employer. More info soon.

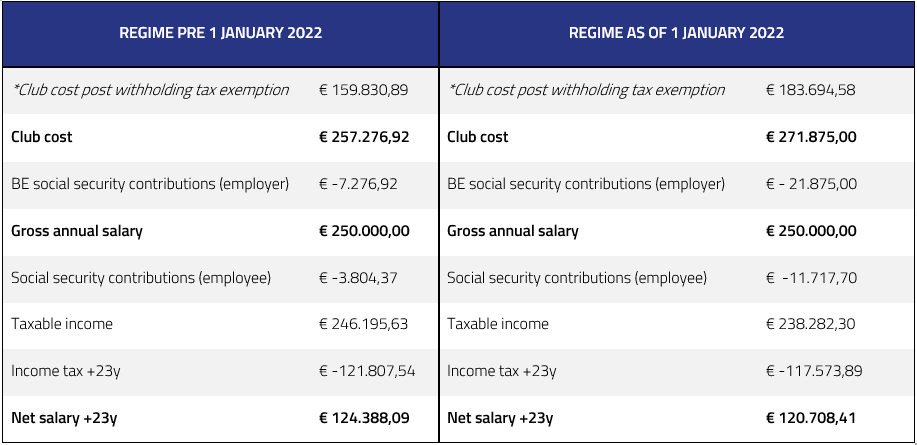

Below table illustrates the impact of the budget reform measures on the company cost in the hands the employer of an athlete taxable in Belgium and subject to Belgian social security. This example applies to an employee with an annual gross salary of EUR 250,000.

For questions, please feel free to contact us:

This email address is being protected from spambots. You need JavaScript enabled to view it.

This email address is being protected from spambots. You need JavaScript enabled to view it.

This email address is being protected from spambots. You need JavaScript enabled to view it.

Tour & Taxis

Havenlaan/Avenue du Port 86C B414

BE-1000 Brussels

T +32 2 421 94 94

info@atfield.be